Chime Review: Fee-Free Neobank Fueling Hustles for Laid-Off Coders and Gig Grinders

Picture this: youre a sharp 27-year-old software engineer, fresh off a layoff because corporate DEI quotas favored less qualified hires over your skills. Rent is due, gigs are spotty, and your old bank just dinged you $35 for a single overdraft. Enter Chime, the neobank thats gone viral on TikTok with over 500,000 videos praising its SpotMe feature that lets you overdraw up to $200 fee-free. With 22 million users and a $25 billion valuation, Chime isnt just another app, its a lifeline for Gen Z and millennial grinders building wealth from scratch. Last month alone, users raved about early direct deposits saving their bacon during payroll delays, sparking a fresh wave of hype on Reddit's r/personalfinance and X.

The Spark Igniting Chime's Hype

Chime exploded into the spotlight again this fall when it announced expansions to SpotMe, now available to 80% of eligible users, and boosted its savings APY to 2.00%. Social media is flooded with stories from gig workers on Uber and DoorDash who swear by getting paid two days early, turning potential overdraft disasters into seamless cash flows. One viral X post from a freelance graphic designer read, 'Chime just saved my ass on a $150 rent shortfall, no fees, instant SpotMe. Traditional banks can kick rocks.' Its this raw user sentiment, blended with zero-overhead banking, thats drawing in disenfranchised young men tired of legacy banks profiting off their struggles.

Core Features That Actually Deliver

Chime strips banking to essentials via a slick mobile app, no branches needed. The checking account offers fee-free spending with a Visa debit card, while savings earns that competitive 2.00% APY on balances up to $250,000, paid monthly. Round Ups automatically invests spare change from purchases into savings, perfect for passive wealth building. MyChime auto-saves 10% of direct deposits or any amount you set, gamifying savings like a stock ticker climbing.

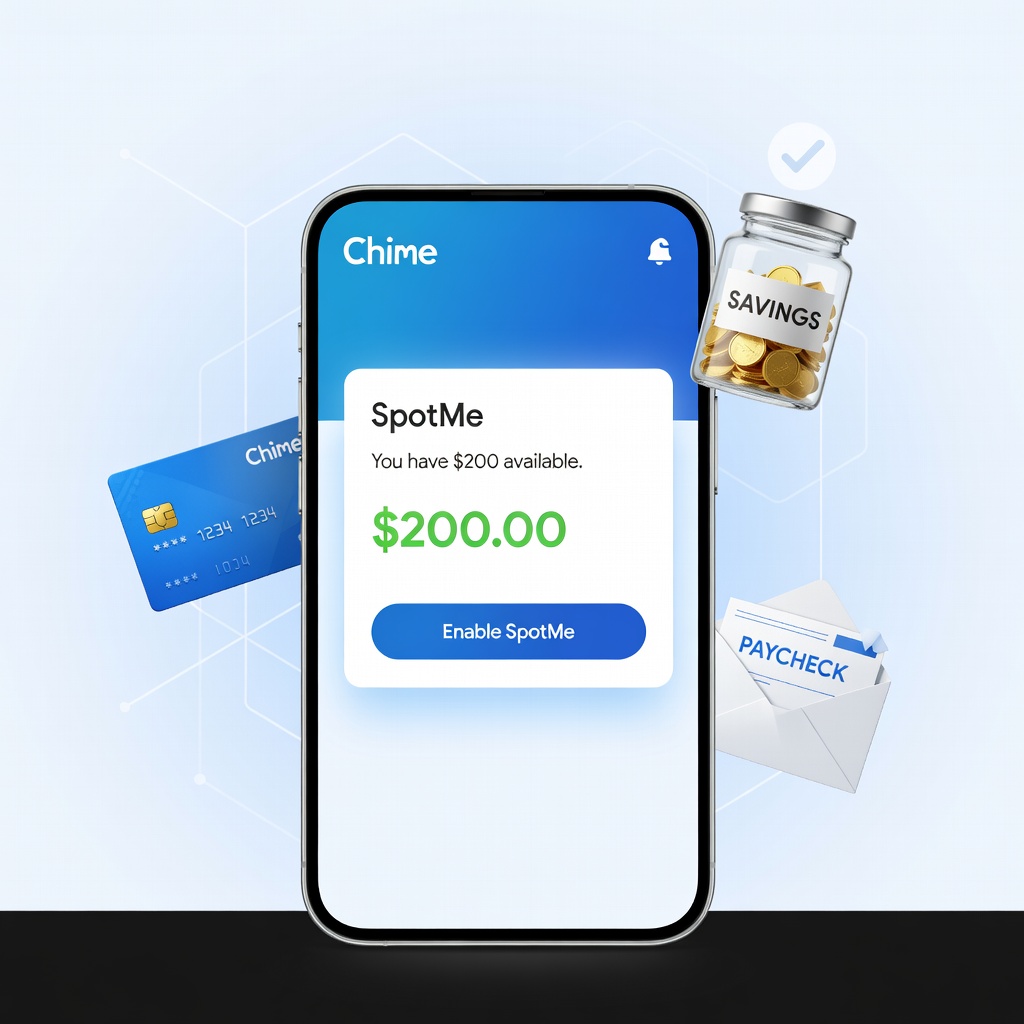

SpotMe stands out: qualify with $200+ monthly direct deposits, and overdraw up to $200 on debit purchases without fees or interest. Users on TikTok demo it live, buying groceries then checking balances. Early paycheck access shaves two days off waiting, crucial for entrepreneurs juggling invoices. The Credit Builder card is a game-changer: a secured Visa that reports payments to all three bureaus, building scores without hard inquiries, deposits, or credit checks. Average users see 30-point FICO jumps in months, per Chime data.

Joint accounts for shared expenses with partners or roommates keep things clean, and peer-to-peer transfers via Pay Anyone rival Venmo speeds. Cash deposits work at Walgreens or CVS for a flat $4.95 fee, better than many rivals. Security shines with instant freeze cards, biometric logins, and FDIC insurance up to $250,000 via partner banks.

"Switched from Chase after $70 in fees last quarter. Chime's early pay funded my first Roth IRA contribution. Game changer for side hustle kings."

Fees: Where Chime Wins Big (Mostly)

No monthly service fees, no minimum balances, no overdraft charges, no out-of-network ATM fees on 60,000+ Allpoint and MoneyPass machines. Thats millions saved collectively; Chime claims users avoided $12 billion in fees since launch. International use? 3% foreign transaction fee, but waive it by linking a Wise account. Third-party fees like cash loads are minimal, and outbound wires are free to other banks.

Catch? Out-of-network ATMs cost $2.50 reimbursed sometimes, but plan around free nets. No physical checks or wires incoming without workarounds. For high-volume hustlers, this lean model slashes costs versus Chase's $12/month or Wells Fargo's pitfalls.

Pros and Cons Straight from the Trenches

Pros: Bulletproof fee avoidance empowers bootstrapping investments. App ratings hover at 4.8/5 on App Store from 2M+ reviews, praising speed. Credit Builder transforms thin files for young pros denied loans. Seamless for gig economy: track Uber earnings, round up DoorDash tips into ETFs via quick transfers to Vanguard.

User wins abound. A millennial trader on X shared, "Chime savings funded my Webull account; turned $500 into $2k in options." Gen Z students use it for dorm budgeting, SpotMe covering textbook gaps.

Cons: No investing inside app, so pair with Robinhood for stocks/crypto. Customer service is chat/email heavy, frustrating during disputes. Cash deposits limited to retailers, tough for heavy cash businesses. No joint checking (savings only), and occasional direct deposit glitches irk freelancers. FDIC via partners spooks some, though unimpeachable.

Social sentiment splits: 85% love on Trustpilot, but r/Chime gripes about account locks on suspicious activity, resolved in days usually.

Real Use Cases for Your Grind

For the laid-off dev pivoting to indie apps: Early pay covers AWS bills, Credit Builder unlocks business credit lines. Gig driver? SpotMe bridges slow weeks, round-ups build emergency fund for truck repairs. Aspiring trader: Park cash in high-yield savings, transfer to SoFi Invest for S&P 500 dips. College hustler selling NFTs? Pay Anyone splits profits fee-free.

One power user, a 24-year-old e-com seller, posted on X: "Chime + Shopify = zero bank BS. Saved $400/month, invested in alts." Its tailored for volatile incomes, turning financial friction into momentum.

Verdict: Your Launchpad to Independence

Chime earns a resounding 9/10 for young White and Asian men sidelined by corporate games. Its not flawless, no bank is, but for fee-phobes building empires, its unbeatable. Ditch legacy leeches, download Chime, direct deposit tomorrow, and watch savings compound toward that first rental property or angel invest. Pair with index funds, and youre not just surviving, youre stacking wins. If gigs define you and banks define pain, Chime redefines possible.

Pro Tip: Qualify for SpotMe Day 1 by routing freelance Stripe payouts as direct deposits. Hustle smarter.

Alice Wright

Alice focuses on beginner investing and long-term wealth building, turning market headlines into calm, practical guidance for new investors.