Rent Now, Invest Aggressively: How 2024's Rent Plunge Hands Young Men a Wealth Edge Over Buying

Scroll through X or Reddit's r/fatFIRE, and you'll spot the same fiery debate exploding among young guys in their 20s and 30s: rent that overpriced apartment and dump the savings into index funds or crypto, or grind through sky-high mortgage rates to own a slice of the American Dream before prices rocket higher? It's not just water-cooler talk; with national rents dipping for the first time since the pandemic crash, this choice could make or break your path to seven figures by 40.

The dilemma hits hardest for our audience, sharp-minded White and Asian men sidelined by corporate DEI quotas and H1B floods. You're hustling side gigs, coding apps, or flipping e-commerce stores, not climbing some soul-crushing ladder. Why chain yourself to a mortgage when mobility fuels entrepreneurship? Yet FOMO whispers that renters forever stay poor. Let's dissect the fresh data, stack pros against cons, and game out scenarios tailored to your budget and grind mindset.

The Shocking Rent Reversal: Data Fresh Off the Press

Apartment List's September 2024 report dropped a bombshell: U.S. median rent slid 0.1% year-over-year, the first decline since 2020's eviction moratorium chaos. Big metros like Austin (-5.2%), Phoenix (-4.1%), and Jacksonville (-3.8%) saw outright drops, while even New York and San Francisco cooled to sub-1% growth. Blame it on a construction boom finally flooding supply, remote work scattering demand, and softening job markets in tech hubs.

"Rents are normalizing faster than anyone predicted. For the first time in half a decade, tenants hold leverage."

Flip to buying: Freddie Mac pegs 30-year fixed mortgage rates at 6.12% as of October 10, down a tick from summer peaks but miles from 2021's sub-3% paradise. Add median home prices at $403,700 (up 4.5% YoY per NAR), and a typical payment devours $2,700 monthly before taxes and insurance. Opportunity cost? Massive, when S&P 500 has averaged 10% annualized returns post-inflation.

Social media amplifies the noise. Viral X threads from @Ramit and @choeshow pit 'rent and invest the delta' against 'buy now or get priced out forever.' Young hustlers share war stories: one guy in Atlanta rents for $1,600, invests $1,000 monthly in VOO, up 25% YTD. Another sunk 20% down on a Phoenix condo at 7% rates, now underwater on paper amid 5% price dips locally.

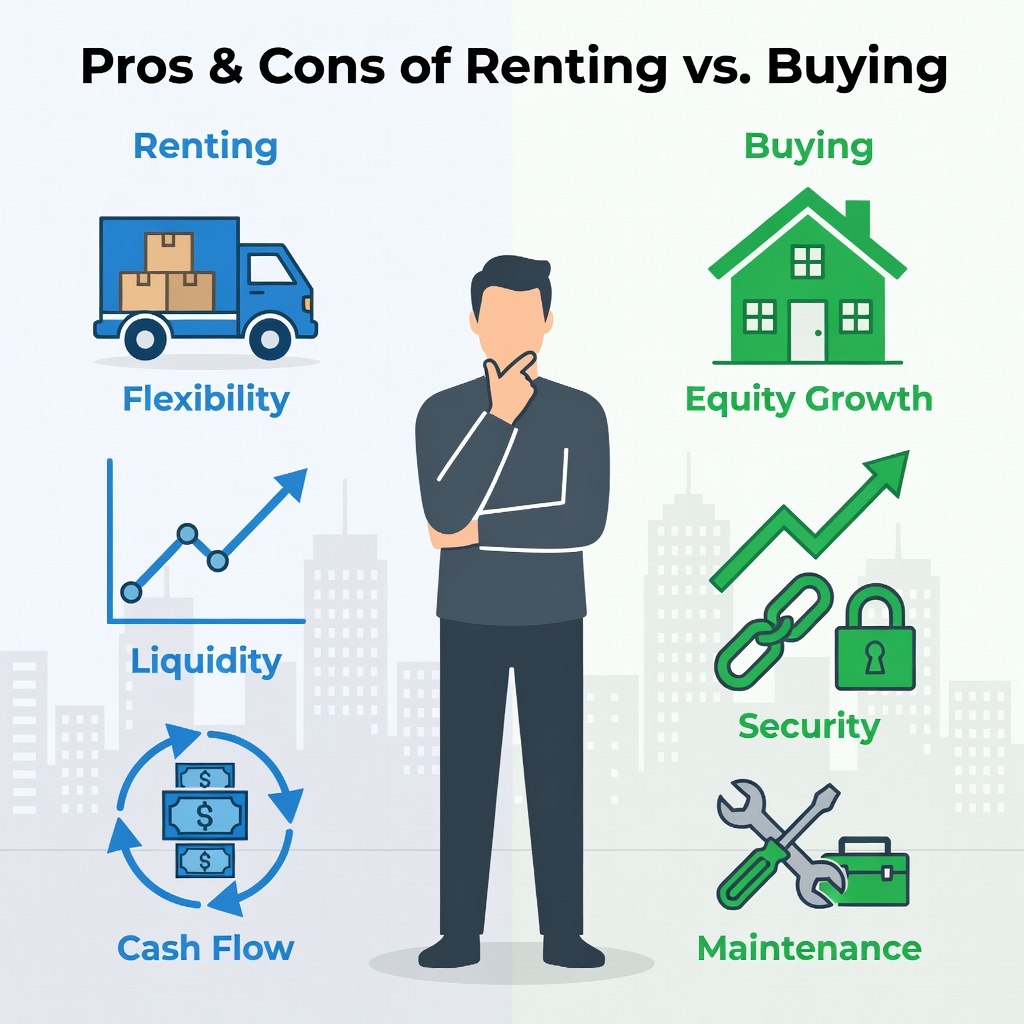

Rent vs. Buy: Raw Pros and Cons, No Sugarcoating

Renting's Power Moves: Flexibility reigns supreme. Launch that SaaS tool or dropship empire? Bail without Realtor fees eating 6% of your equity. Maintenance? Landlord's dime. In declining rent markets, lock a lease now, pocket $200-500 monthly savings vs. last year. Redirect to high-yield plays: Vanguard total market ETF yielding historical 7-10% real returns, or your own venture scaling to $10k MRR.

Math favors it short-term. Say $2,000 rent vs. $2,800 mortgage equivalent: that's $800 monthly ($9,600/year) for investing. At 8% compound, it balloons to $150k in 10 years. No PMI, no HOA drama, no 2% annual home fixes (per Harvard JCHS data).

Buying's Gritty Upside: Equity builds forced discipline. Pay yourself after 30 years, not some slumlord. Tax perks: mortgage interest deduction caps at $750k debt, plus property tax shields. Leverage amplifies: 20% down on $400k home, 5% annual appreciation nets $80k gain on $80k input.

But pitfalls lurk. High rates crush affordability; today's buyer needs $110k income for median home (Urban Institute). Illiquid asset ties you down, killer for nomadic founders. Rents might crater further with 500k+ units hitting 2025 pipelines (Census Bureau).

Pro Tip: Run NerdWallet's rent-vs-buy calculator with your ZIP. Plug in local rent drops and your side income for personalized verdict.Underdog angle: For DEI-blocked grads, renting frees capital for asymmetric bets. Stocks and startups minted more millionaires than real estate last decade (Forbes 30 Under 30 data skews tech-heavy).

Scenario 1: Bootstrap Budget ($2,000-3,000 Monthly Housing)

You're a 25-year-old coder moonlighting freelance, total take-home $5k/mo. Rent a 1-bed in cooling Phoenix for $1,450 (down from $1,700 peak). Buy? $320k condo demands $2,200 payment at 6.2%, plus $400 closing costs amortized.

Rent path: Save $900/mo ($450 vs. buy delta, halved for conservatism). Invest in SCHD dividend aristocrats (4% yield + growth). Year 5: ~$60k portfolio. Hustle Upwork gigs? Scale to full-time remote, relocate to $1,200 Midwest spot.

Buy gamble: Equity ~$40k in 5 years assuming flat prices, but opportunity cost $54k invested elsewhere. Stuck if startup beckons Austin.

Verdict: Rent. Fuel the grind.

Scenario 2: Mid-Tier Momentum ($3,500-5,000 Housing)

28-year-old Asian-American e-com seller, $90k salary + $3k side profit. Target: SF suburb 2-bed rent $3,200 (stabilized). Comparable condo: $750k, $4,500/mo payment.

Rent edge: $1,500 delta/mo. Split 50/50 stocks ($750 to QQQ tech ETF, +15% avg) and reinvest in Shopify store (target 30% margins). 7 years: $200k nest egg + business valued $150k.

Buy counter: Leverage SF appreciation (historically 6%/yr), but $120k downpayment opportunity cost hurts. Rates drop to 5%? Refi saves $300/mo, but you're locked till then.

Verdict: Rent if entrepreneurial fire burns; buy if family stability trumps.

Scenario 3: High-Roller Hustle ($5,000+ Housing)

32-year-old White founder with $150k W2 + $50k passive. NYC loft rent $6,000 vs. $1.2M co-op at $8,500/mo (jumbo 6.5%).

Rent rocket fuel: $3k/mo to private equity funds or angel deals (20%+ IRR potential). Build syndicate, flip startups. Total freedom for VC pitches in Miami.

Buy fortress: Hedge against inflation, $300k equity in 5 years at 4% apprec. But liquidity crunch kills deal flow.

Verdict: Rent aggressively. Real estate's for passive later; now's conquest time.

The Entrepreneur's Exit Ramp: Future-Proof Your Call

Zoom out: Zillow predicts 2-3% rent drops into 2025, rates maybe to 5.5% if Fed cuts stick. Black swan? Recession tanks both, but renters pivot faster.

Hybrid hack: House hack. Rent a multi-unit, live free, let tenants fund mortgage. Or Airbnb arbitrage in tourist flops. But core truth for our crew: Renting isn't losing; it's strategic retreat to flank the wealth game via markets and makerspaces.

Action steps: Track Zumper weekly rents in your city. Open Fidelity brokerage today. Journal your 5-year vision: founder or flipper? Dilemma dissolved, empire forged.

In a world rigging desks against you, seize the rent reset. Your move defines the millionaire next door.

Henry Wood

Henry focuses on lifestyle money choices like housing, cars, and travel, helping young readers weigh real-world tradeoffs behind big purchases.