Rent or Buy? Falling Mortgage Rates Spark Fierce Debate Among Young Hustlers Weighing Mobility vs. Wealth Building

Scroll through X or Reddit's r/fatFIRE, and you'll spot the same fiery thread exploding weekly: should a 28-year-old software dev lock in a mortgage now, or keep renting to stay nimble for the next startup pivot? With 30-year fixed rates tumbling to 6.32 percent last week per Freddie Mac data, the rent-vs-buy calculator is flipping scripts in major metros. Rents, meanwhile, hover near all-time highs at a national median of $1,670 according to Apartment List's September report, flat year-over-year but squeezing budgets in tech hubs like Austin and Denver. For young White and Asian guys iced out of corporate tracks by DEI quotas and H1B floods, this isn't abstract math. It's a fork in the road between forced savings through equity and the freedom to chase entrepreneurial moonshots without house poor regrets.

The Fresh Data Drop Igniting the Firestorm

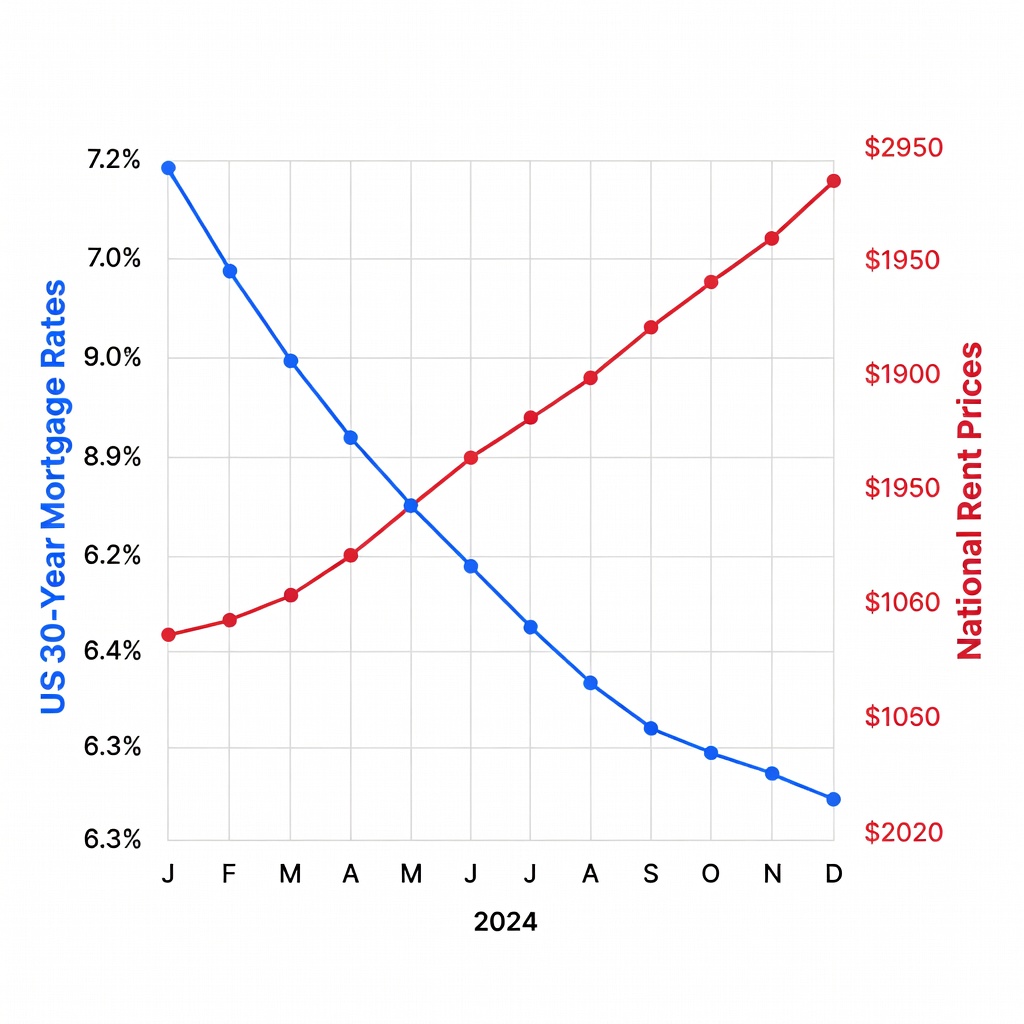

Freddie Mac's October 17 update slashed average 30-year rates to 6.32 percent, the lowest since April, down from summer peaks above 7 percent. That's a game-changer for affordability. On a $400,000 home with 10 percent down, monthly principal and interest drops from $2,661 at 7 percent to $2,295 at 6.32 percent, shaving over $4,000 yearly before taxes and insurance. Redfin reports existing home inventory up 25 percent year-over-year, easing bidding wars that priced out first-timers.

Rent trends tell a different tale. Zillow's Observed Rent Index pegged national average at $2,020 in September, up 3.2 percent annually, with Sun Belt cities like Miami (7.6 percent jump) and Phoenix leading surges. In high-demand spots favored by remote coders and indie devs, such as Nashville or Raleigh, two-bedroom units command $2,200-plus. Social media erupts with screenshots: a viral X post from @FinanceBroNYC last week contrasted his $3,200 Brooklyn rent hike notice against a co-worker's $2,800 mortgage payment on a similar square footage nearby. Comments piled on: 12K likes debating if renting lets you deploy cash into S&P 500 ETFs yielding 10 percent average returns versus home appreciation stuck at 3 percent lately.

Renting: Pros, Cons, and the Hustle Edge

Pros: Ultimate flexibility rules for the entrepreneurial grind. No skin in the real estate game means you can relocate to Silicon Valley for that AI gig or bootstrap a SaaS in Bali without selling fees eating 6 percent. Maintenance headaches? Landlord's problem. That frees bandwidth for side hustles like dropshipping or crypto trading. Opportunity cost shines: park your would-be down payment in VOO and compound at historical 10 percent. A $80,000 down payment grows to $211,000 in 10 years versus a home potentially flatlining amid recessions.

Cons: Rent inflation erodes wealth stealthily. Today's $2,000 lease balloons to $3,000 in five years at 5 percent hikes, per historical BLS data. Zero equity buildup means you're funding someone else's portfolio. Tax perks? Zilch compared to mortgage interest deductions. And psychologically, perpetual renter status stings for guys building legacies, especially when peers post renovation flexes.

In Reddit's r/personalfinance, a thread with 5K upvotes last month featured a 26-year-old Asian dev in Seattle: "Rented five years, invested diffs in tech stocks. Up 150 percent. House poor friends underwater." Counterposts warn of black swan rent spikes during job hunts.

Buying: Pros, Cons, and Forced Discipline

Pros: Leverage amplifies wins. With rates dipping, lock in fixed payments while rents float upward. Homeownership builds equity stealthily: principal paydown plus 4 percent annual appreciation (Case-Shiller Q2 average) turns $400K purchase into $600K asset in a decade. Uncle Sam sweetens with deductions up to $750,000 debt. Stability anchors family starts or home offices for consulting empires. For disenfranchised talent, it's a hedge against inflation and a wealth transfer tool, bypassing corporate wage suppression.

Cons: Upfront cash burn: 20 percent down ($80K) plus closing costs ties up seed capital for ventures. Illiquidity traps you if the next opportunity demands a cross-country move. Rates, though falling, remain double pre-2022 levels, inflating payments 50 percent over 3 percent era. Repairs, HOAs, property taxes add $500 monthly unpredictability. Zillow's rent-vs-buy tool shows renting cheaper in 40 of 50 metros for starter homes under $500K.

X user @EntrepreneurDad nailed it: "Bought at 6.8 percent. Equity up $120K in two years. Renters still bleeding." But replies highlight divorce risks or market crashes wiping gains.

Scenario Breakdown: Tailor to Your Grind

Budget Hustler ($60K income, $1,500 monthly housing max): Rent wins. A $350K condo demands $70K down (impossible without loans), pushing payments to $2,200 with PMI. Rent a $1,400 one-bed in growing suburb like Boise, invest $10K yearly in index funds. Mobility for job hops or skill upgrades trumps marginal equity.

Mid-Tier Climber ($120K income, tech salary, $3,000 budget): Buy edges out in suburbs. $450K townhome, 15 percent down ($67.5K), payment $2,600. Rents match or exceed at $2,800. Equity builds while stocks ride bull market. Ideal for settling post-corporate exit, flipping to VRBO later.

High-Roller Entrepreneur ($250K+ from SaaS/exits, $5K+ budget): Buy aggressively. Snag $800K fixer-upper in appreciating hood like Atlanta outskirts. Payments $4,500 fixed, rents $6K equivalent. Use home equity line for business scaling post-year three. Leverage beats liquidity for legacy builders.

Tweak for priorities: family-focused? Buy. Nomad coder? Rent and Vanguard. Data-driven? Plug your zip into NY Fed's calculator; it favors buying in just 15 states now.

The Verdict for Wealth Warriors

This dilemma boils down to your runway. Falling rates tilt scales toward buying for stability and inflation-proofing, especially if entrepreneurship demands a base. Yet renting fuels velocity for those dodging golden handcuffs. Hybrid hack: house hack with roommates, Airbnb spare room, turning liability to asset. Whatever path, act asymmetrically: deploy non-housing cash into dividend aristocrats or your own IP. Social media noise fades; your 10-year net worth won't. Ditch analysis paralysis, run projections, and own the decision that aligns with escaping the rat race on your terms.

"Rents are the new student loans: endless payments, zero asset." Anonymous X fintech influencer, 20K likes

Henry Wood

Henry focuses on lifestyle money choices like housing, cars, and travel, helping young readers weigh real-world tradeoffs behind big purchases.