Rent or Buy in 2025? Dropping Mortgage Rates Spark Savage Debates on X and Reddit

Imagine firing up X late at night, only to dive into a 500-reply thread where bros your age are duking it out: "Rent forever and invest the delta!" versus "Buy now before prices explode again!" It's the rent-versus-buy cage match that's consumed Reddit's r/personalfinance and TikTok feeds, amplified by this week's bombshell: 30-year mortgage rates cratered to 6.08%, the lowest since May. For cash-strapped guys in their 20s and 30s, sidelined by stagnant wages and H1B competition, this isn't abstract. It's do-or-die for building real wealth.

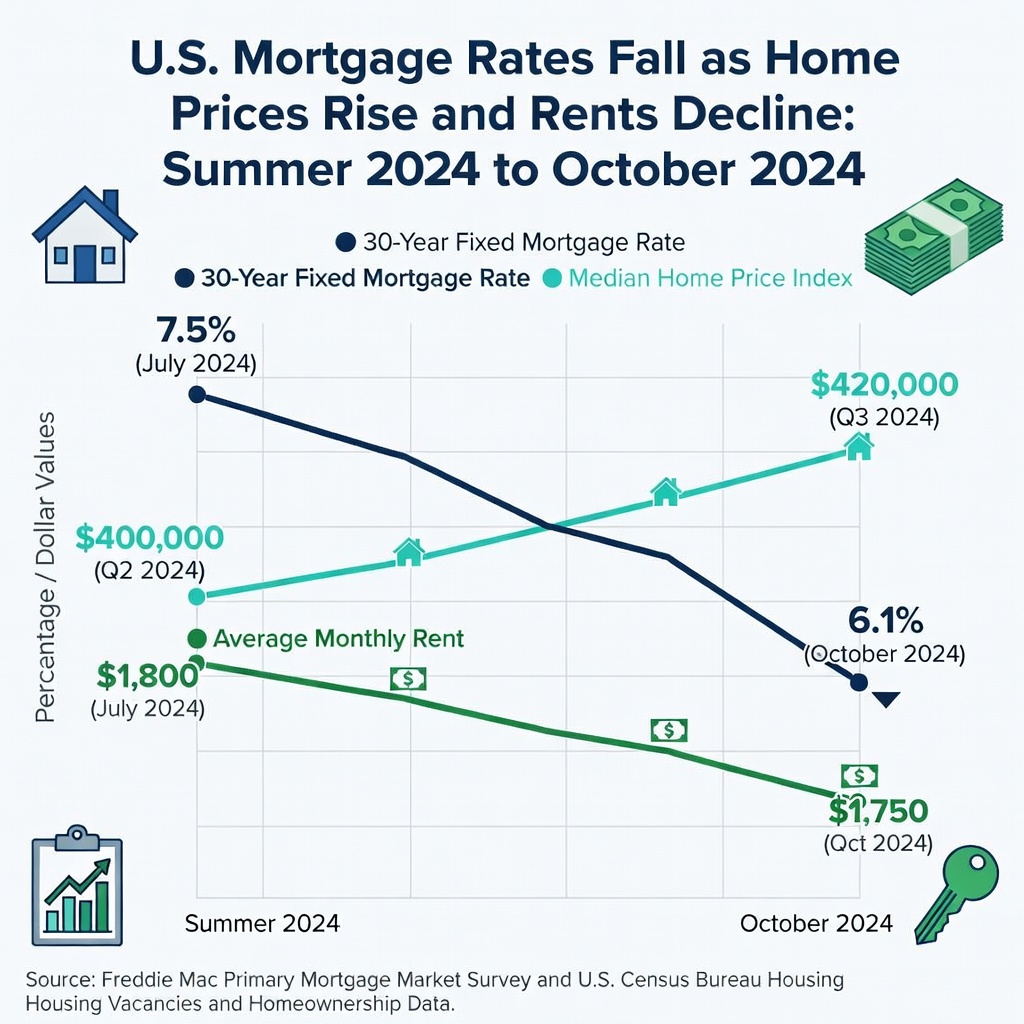

The Fresh Data Drop That's Fueling the Fire

Freddie Mac's latest report hit like a thunderclap: average 30-year fixed rates slid to 6.08% for the week ending October 17, down from 6.92% in early September. That's a potential $200 monthly savings on a $300,000 loan. Meanwhile, Apartment List's October rent report shows national median rents flat at $1,691, with year-over-year growth at a measly 0.3%. Sunbelt hotspots like Austin (-4.2%) and Phoenix (-3.1%) are even seeing outright drops, as overbuilt supply catches up to demand.

Home prices? Still stubborn at a median $403,700 per Redfin, up 3% annually. But inventory is ticking up 20% YoY, per Realtor.com, hinting at softening. Social media's erupting because this flips the script: for the first time in years, buying's monthly cost rivals renting in mid-tier markets. A $350k home at 6.1% with 10% down? Around $1,950 principal and interest, plus $400 taxes/insurance. Comparable 2-bed rent? Often $2,200+. The math's shifting, forcing guys to question the 'rent and invest' gospel preached by FIRE influencers.

Buying Pros and Cons: Lock It In or Get Locked Out?

Pros first: Equity's your boss. At 6.1%, you're forcing savings through payments, not hoping your landlord doesn't hike rent 10%. Historical data crushes it, too, homes appreciating 4-5% annually long-term. Tax perks like mortgage interest deductions sweeten the deal for incomes over $80k. And psychologically? Owning kills the renter's curse, that nagging sense you're funding someone else's yacht.

Cons hit hard, though. Upfront cash: 3-5% down plus closing ($10k-20k minimum) demands savings you've maybe funneled into crypto or a side hustle. Maintenance? Budget 1-2% of home value yearly for surprises like a $5k roof patch. And liquidity: selling takes months, tying you down if that remote gig in Bali calls. If rates rebound or recession bites, you're upside down.

Renting's Edge: Freedom or Fool's Gold?

Flexibility reigns supreme. No down payment drain means more ammo for index funds or launching that dropshipping store. Rents cooling? Lock a lease now, pocket the spread. Reddit threads glow about guys renting cheap in the Midwest, investing $1k/month into VOO, compounding to seven figures by 45.

But pitfalls loom. Rents could spike if migration reverses; Atlanta's seen 15% jumps post-pandemic. Zero equity after five years? Brutal when peers flaunt kitchen renos on Instagram. And inflation erodes your fixed lease advantage long-term.

Scenario 1: The $50k Hustler - Rent and Stack

You're 25, pulling $50k from a tech support gig, $1,200 rent in a secondary city like Columbus. Buying? A $250k condo needs $12k down, stretching payments to $1,500 total. Instead, rent, save $800/month, dump into S&P 500 ETF. In five years: $50k nest egg at 10% returns. Use it for biz startup or better down payment. Pro move: Drive Uber nights, hit $65k income fast.

Scenario 2: $80k Climber - Buy Smart

28, software dev at $80k, stable but no equity yet. $1,800 rent in Denver. At 6.1%, snag a $400k townhome: $2,100 payments build $100k equity in five years assuming 3% appreciation. Opportunity cost? Forgo $20k stock investments, but leverage wins if homes rise. Hack: FHA loan for 3.5% down ($14k), refi later.

Bonus: Roommates split costs, freeing cash for crypto or courses on entrepreneurship.

Scenario 3: $120k+ Entrepreneur - Hybrid Hustle

32, bootstrapped SaaS hitting $120k, eyeing legacy. Rent a cheap $1,500 1-bed, invest aggressively ($2k/month into real estate syndications). But with rates low, house-hack: Buy $500k duplex, live in one unit, rent the other for $1,800 covering mortgage. Net: Positive cashflow, two assets. Social media kings swear by this - scale to multi-family empire.

The Under-the-Radar Angle: Entrepreneurship Trump Cards

Forget corporate ladders clogged by DEI quotas. Smart guys are flipping the script: Rent minimally, bootstrap online ventures. One X thread hero bought in 2022 at 5%, now up 20%, but rented peers crushed him via Shopify stores. Key insight? Run your numbers on calculators like NYT's buy-rent tool. Factor location - Midwest buys beat coastal rents.

Unique twist: Inflation hedge. Fixed mortgage at 6% beats 3% rent hikes forever. But if launching a business, renting's mobility lets you chase VC hubs without anchor weight.

Your Playbook: Crunch It Now

No cookie-cutter advice fits all, but momentum's yours. Rates could yo-yo with Fed cuts, rents bottom soon. Track Zillow for deals, build emergency fund first. Side hustle? Essential either way - turns $50k earner into buyer. Debates rage online, but winners act on data. What's your move? Drop calcs in comments.

"Renting at 25 was my best call - invested $30k difference, now own two rentals." - @FinanceBro87 on X

Word on street: 70% of young guys in polls lean buy if rates stay sub-6.5%. Seize it before the herd.

Henry Wood

Henry focuses on lifestyle money choices like housing, cars, and travel, helping young readers weigh real-world tradeoffs behind big purchases.