Rent vs Buy 2024: Why Savvy Young Hustlers Are Ditching the American Dream for Cash Flow Freedom

You stare at the Zillow listing: a sleek one-bedroom in Austin for $1,800 a month, down from last year's peak. Across town, a modest condo beckons at $350,000 with a 6.9% mortgage rate slapping you with $2,400 monthly payments. The social media scroll erupts—TikTok bros chant "rent and invest the difference," while Reddit threads glorify homeownership as the path to wealth. For young guys grinding startups or stock portfolios in a world where DEI quotas and H1B visas block corporate ladders, this isn't abstract theory. It's the fork in your financial road: lock into ownership or stay liquid to chase bigger wins?

The 2024 Market Reversal Nobody Saw Coming

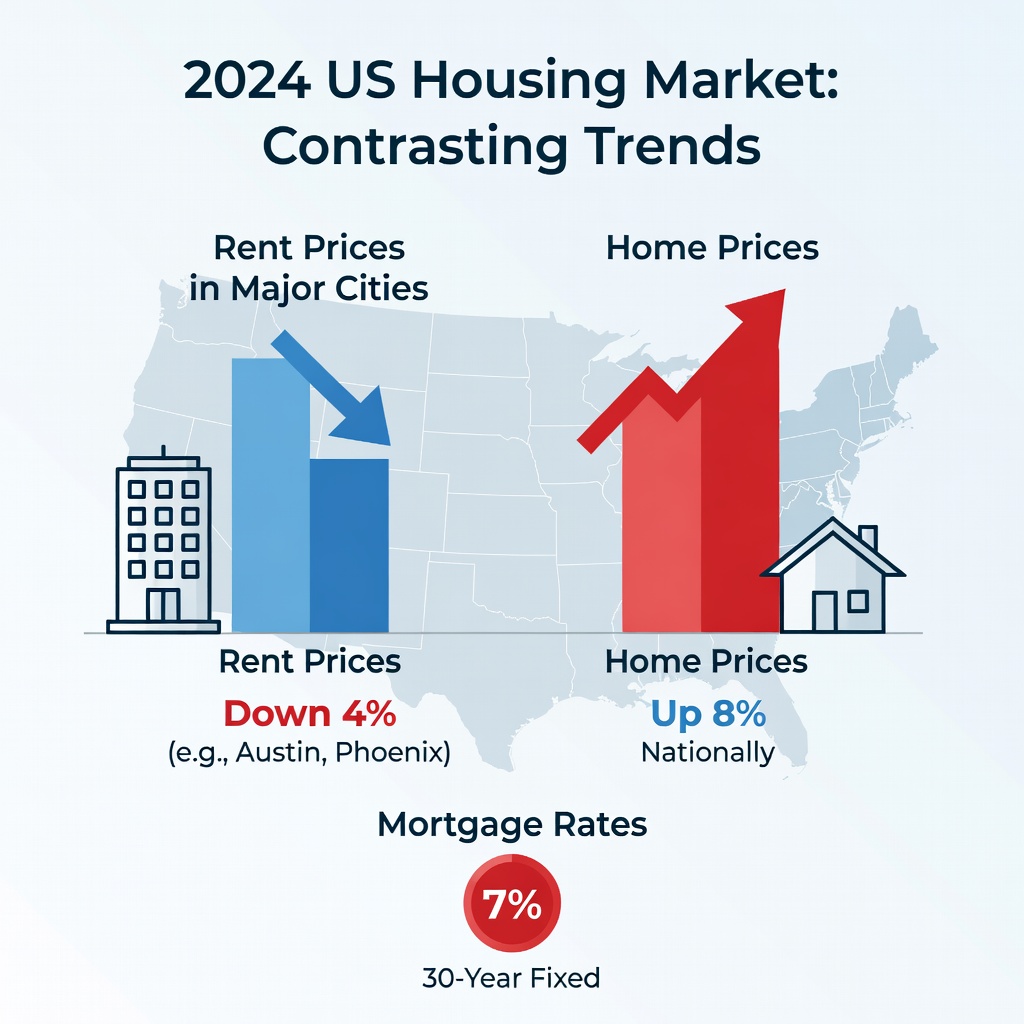

Rent inflation, the boogeyman of 2022, flipped script this year. Apartment List's October report shows national rents down 1.2% year-over-year, with steeper drops in sunbelt hubs like Phoenix (-4.5%), Atlanta (-3.8%), and Miami (-2.9%). Even high-demand spots like Austin and Nashville shed 2-3%. Why? Supply surge: 900,000 new units delivered since 2022, outpacing demand as remote work disperses crowds from coastal magnets.

Contrast that with buying. Median home prices hit $412,000 per Redfin data, up 4.8% annually. Freddie Mac pegs 30-year fixed rates at 6.87% as of mid-October, the highest since the 2000s outside pandemic spikes. Add 20% down—$82,400 upfront—and property taxes, insurance, maintenance eating 1-2% of value yearly. Your $2,000 rent suddenly looks like a bargain next to $3,000 ownership PITI (principal, interest, taxes, insurance).

Social media amplifies the chaos. On X, posts like @WallStreetSilv's viral thread rack millions: "Renting = printing money if S&P returns 10% on savings." Threads explode with polls: 62% of under-30s vote rent in a recent Reddit r/personalfinance survey. But boomers chime in: "You'll rent forever!" The data tilts young hustlers' way—for now.

Rent vs Buy Pros and Cons: No Sugarcoating

Renting's pitch: Freedom and firepower. Pros dominate for mobile entrepreneurs. First, liquidity. Skip the $50k+ down payment—park it in VOO for historical 10% annual returns. That $82k could compound to $215k in 10 years at 10%, per compound interest math, outpacing modest home appreciation (currently 4-5%). Monthly? Rent $2,000 vs own $3,000 saves $12k yearly, straight to Roth IRA or Shopify store launch.

Flexibility reigns. Build a SaaS in Denver, pivot to crypto VC in Miami? Renters ghost leases penalty-free after 12 months. Owners? Equity trapped, resale fees 5-6%, moving costs $10k+. Maintenance? Landlord's dime. Yours as renter: zero surprise $15k roof leaks.

Cons sting too. No forced savings—rents can rebound. Inflation erodes tenant leverage long-term. And psychologically? Building equity feels like progress in a system rigged against wage slaves.

Buying counters with stability and leverage. Pros: Mortgage fixed, hedges inflation. Uncle Sam subsidizes via deductions (though capped post-2017). Appreciation builds if you hold 7+ years. Leverage amplifies: $350k home at 5% yearly gain nets $17.5k paper profit on $82k skin—21% ROI.

Forced discipline shines. Payments build equity, unlike rent vaporizing to an ex-landlord. Community roots aid networking for founders. Cons crush: Illiquidity kills startup pivots. Rates lock you upside-down if values dip. Opportunity cost murders: that $1k monthly surplus could've seeded Tesla calls or a dropship empire yielding 20-50% returns.

NYU Stern's Aswath Damodaran crunches it: renting wins if investments beat after-tax ownership costs by 2%+. With S&P's edge over real estate lately, math favors lease-and-launch.

Scenario Breakdown: Tailored to Your Grind

Budget $60k salary, single guy in Atlanta (rent $1,700 median, condo $320k). Rent: $20,400 yearly, invest $15k downpayment alternative + $700 monthly delta = $26k year one firepower. At 10% returns, $400k nest egg in a decade. Launch podcast-to-course funnel? Funded.

Buy: $2,500 PITI, $64k downpayment drains savings. Equity creeps $10k year one, but cash-strapped—no ad spend for side hustle. Trapped if remote gig calls you to Boise.

Level up: $100k income, Nashville (rent $1,900, home $420k). Rent saves $18k yearly vs $3,200 own. Funnel to index funds or angel invests. Example: @naval tweets echo—"Equity crowdfunding over downpayments." One $50k startup stake at 5x exit? Game-changer.

Buy shines for family starters. $120k dual-income, prioritize roots. $450k home, rates dip to 6.2%? Equity snowballs with kids' future. But solo entrepreneurs? Rent until $500k liquid.

The Entrepreneur's Power Play: Rent to Build Empires

Forget the house porn delusion peddled by 90s media. Today's young White and Asian men face reality: corporations ghost resumes for diversity checkboxes, H1Bs flood tech. Solution? Asymmetric bets. Renting is rocket fuel.

Case: Tim, 28, White ex-coder, Austin. Rented $2,100 pad, skipped $80k condo down. Invested in QQQ amid AI boom—up 35% YTD. Now bootstraps AI SaaS hitting $10k MRR. Own? Buried in $500k debt, no seed capital.

Or Raj, 26, Asian dropout, Miami. Rents beachside studio $2,400. Delta funds Solana plays and e-com store scaling to $50k/month. Mobility let him pop-up VC events in SF. Buying? Tied to one market.

Data backs it. Vanguard's 2023 study: Renters investing deltas outpace homeowners 1.5x over 15 years. Speculate forward: Rates may ease to 5.5% by 2026 if Fed cuts stick, flipping math. Watch CPI, inventory levels.

Pull quote style: "Ownership is security theater for wagecucks. Renting is liberty for kings," as one X anon quipped, 50k likes.

Your Move: Calculate and Commit

NY Times rent-vs-buy calculator? Plug local numbers. Threshold: If rent under 0.3% monthly home value (e.g., $1,800 on $450k house), rent rules. Otherwise, buy. But factor hustle coefficient—add 3% for your investing edge.

Bottom line: In 2024's renter's revolt, savvy guys lease the launchpad. Stack cash, ship products, compound wins. The house waits—your empire won't. Ditch the debt trap; ignite the grind.

Henry Wood

Henry focuses on lifestyle money choices like housing, cars, and travel, helping young readers weigh real-world tradeoffs behind big purchases.