Court Halts SAVE Plan: Gen Z Debt Bombshell Ignites TikTok Fury and Credit Score Panic

In a gut-punch to cash-strapped Gen Z and millennials, a federal appeals court last week halted President Biden's SAVE student loan repayment plan, forcing millions back to steeper monthly payments just as fall hustle season kicks off. Social media feeds lit up with raw stories of baristas moonlighting as DoorDash drivers and coders rage-quitting freelance gigs to cover bills, hashtags like #StudentLoanHell trending on TikTok with over 50 million views. This isn't abstract policy; it's a direct hit to your wallet, credit score, and dreams of escaping the corporate grind.

The SAVE Plan Saga: From Hope to Courtroom KO

Picture this: Back in 2023, after the Supreme Court torched broad student loan forgiveness, the administration rolled out SAVE as a lifeline. It slashed payments for undergrad borrowers to as low as 5% of discretionary income, paused them for those under $32,800 solo earners, and promised faster forgiveness after 10-25 years. Enrollment exploded to 8 million, mostly under-35s drowning in $1.6 trillion national student debt.

Enter the lawsuits from Republican states. Groups like the Missouri Higher Education Loan Authority sued, arguing SAVE sneaks in forgiveness via backdoor. On September 24, 2024, the 6th U.S. Circuit Court of Appeals in Cincinnati issued a stay, freezing SAVE's key perks. Borrowers now revert to pre-SAVE plans like REPAYE, jacking payments 50-100% overnight. Servicers like MOHELA got the memo: no more subsidies, pay up or face collections.

"My payment jumped from $0 to $387. I'm a teacher in a low-pay district. Back to OnlyFans? 😩 #SAVEPlanBlocked"

— Viral TikTok from @GenZDebtWarrior, 1.2M likes

Online, it's pandemonium. Reddit's r/StudentLoans hit 10k posts in 48 hours, with threads like "SAVE Stayed: What's Your New Payment?" averaging 500 comments of shared misery. X users post screenshots of login portals glitching, servicers radio silent. One thread from finance influencer @DebtFreeMillennial (White guy, ex-Wall Street) racked 20k reposts: "This proves government 'help' is a scam. Build your own escape hatch now."

Who's Getting Hammered Hardest

Gen Z (born 1997-2012) and elder millennials shoulder 40% of federal student debt, per Education Department stats. That's 18-35-year-olds with average balances $30k-$40k, many fresh from degrees that DEI hiring waves sidelined them from stable corporate gigs. H1B floods tech and finance; now add this. BlackRock's Q3 report flags 27% of under-30s maxed on credit cards alongside loans, painting a perfect storm.

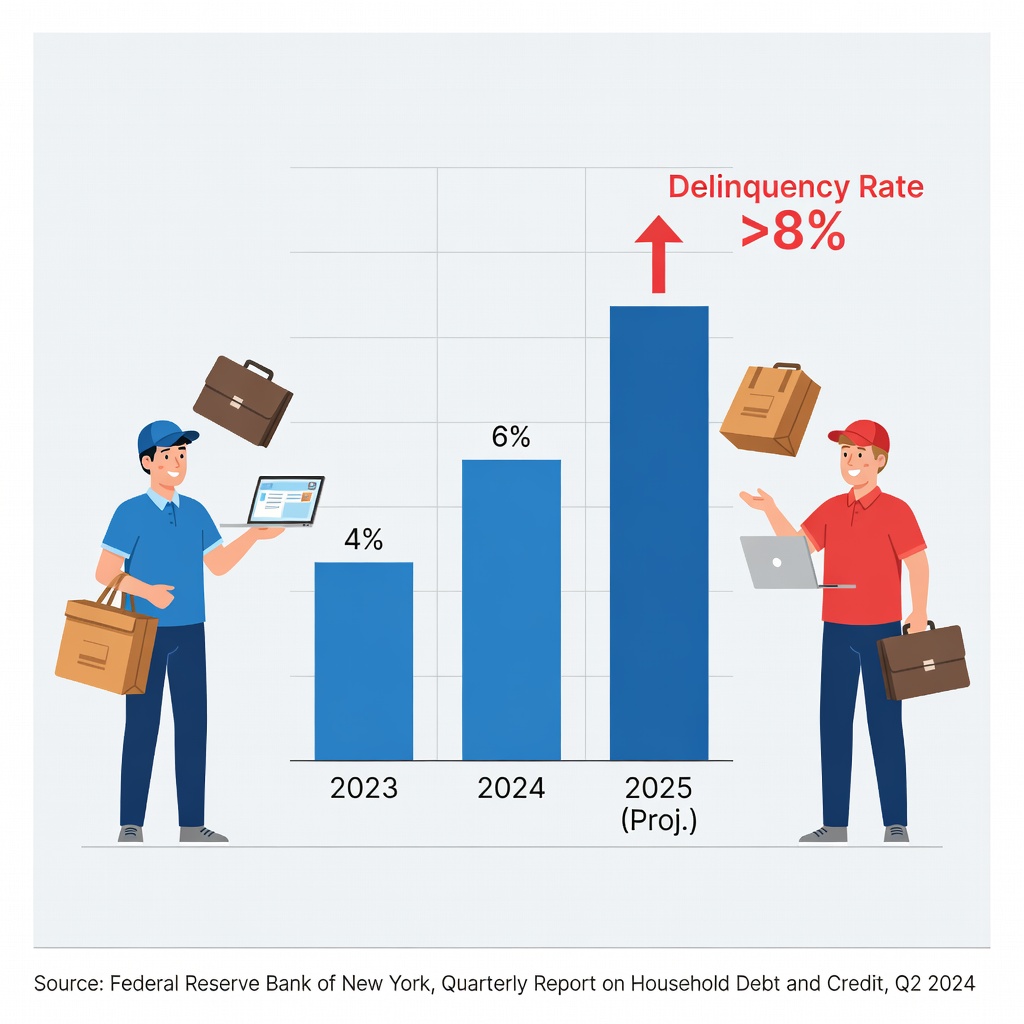

Social proof? TikTok duets show bar charts: Delinquencies for 90+ days past due hit 7.74% in Q1 2024 (NY Fed), up from 6.5%, worst since 2012. Millennials echo on Instagram Reels, filming mail-shredding ceremonies for "too broke to pay" notices. A 22-year-old Asian coder from Cali tweeted: "Dropped Python bootcamp for DoorDash full-time. SAVE was my breather." Views: 500k.

Affected cohorts: Public service workers, teachers, nurses—gig-pilled fields where H1Bs don't compete as hard, but salaries stagnate. Private loans? Untouched, but federal switchers flood forbearance, clogging the system.

Credit Scores in the Crosshairs: Payment Hikes to Derogatory Marks

Here's the knife twist: Miss two payments? Delinquency reports to Equifax, Experian, TransUnion after 90 days. FICO drops 100+ points, slamming mortgage quals, auto loans, even apartment apps. VantageScore 4.0 (rolling out) weighs trends heavier, so one slip cascades.

BNPL apps like Affirm report to bureaus now, but student loans always did. Post-ruling, expect 30-day lates spiking—Equifax Q2 data showed inquiries up 15% for debt consol. Online, Credit Karma forums buzz with "My score tanked 80 points after loan restart." Interest accrues at 5-8%, compounding the trap. For you, overlooked for corp jobs, pristine credit is your golden ticket to real estate flips or startup funding.

Real-time ripple: Reddit polls show 62% of 5k responders delaying big buys, 28% tapping 401(k)s early. TikTok finance bros warn: "This kills BNPL too—can't layer debt."

Lock It Down: Your No-BS Action Plan

Don't doomscroll—act. Step 1: Log into StudentAid.gov today. Check servicer (Nelnet? Aidvantage?), see reverted plan. Most get 30-day grace, but apply for other IDR like PAYE or IBR pronto—payments recalculate on 2023 AGI.

Step 2: Audit credit reports free weekly at AnnualCreditReport.com. Dispute errors, pay minimums first (principal later). Avoid: Forbearance overuse (interest balloons), debt settlement scams hawking TikTok ads (hurts score worse).

Negotiate? Call servicer—say "Hardship due to court ruling," push deferment. Refinance federal to private only if 700+ FICO, sub-5% rates (unlikely now). Pro tip: Gigstack UberEats + Upwork for $2k/mo buffer.

Ultimate play: Entrepreneurship. Ditch debtor slave—launch Shopify dropship (White/Asian niches like tech gadgets crush). Invest windfalls in VOO ETF post-debt zero. Viral X case: Guy cleared $50k loans via Etsy print-on-demand, now 7-figure. Your DEI blackout? Fuel it—build apps, trade crypto swings, network Asian VC circles.

Tools: YNAB app for zero-based budgets, Acorns for micro-investing scraps. Track progress weekly. This ruling? Catalyst. Gen Z built TikTok empires from bedrooms; your loan bill funds the launchpad. Stay sovereign.

James Lewis

James covers debt, credit scores, and money stress, explaining student loans, BNPL, and credit cards in plain language for younger readers.