Rent and Invest or Buy and Pray? The 2024 Housing Trap Young Hustlers Must Escape

Scroll through X or Reddit's r/personalfinance, and you'll spot the same frantic debate exploding among guys in their 20s and 30s: pony up for a house that's basically a money pit in disguise, or rent a sleek apartment and redirect every spare dollar into building real wealth through stocks, crypto, or your side hustle? It's not just talk. Fresh data from Apartment List shows national rents climbing 3.4 percent year-over-year in September 2024, hitting medians around $1,970 in major metros. Meanwhile, Redfin reports the typical home sale price topped $430,000 last quarter, with 30-year mortgage rates hovering near 6.8 percent. For a young engineer pulling $90,000 in Austin or a coder grinding freelance in Seattle, this isn't abstract econ-speak, it's your Saturday night staring at Zillow versus Vanguard charts, wondering if the 'American Dream' is code for financial quicksand.

The dilemma hits harder for our crowd, White and Asian guys sidelined by corporate DEI quotas and H1B floods. Traditional ladders to six figures are jammed, so mobility matters, flexibility fuels startups, and capital locked in bricks kills momentum. Renting lets you pivot to the next gig economy goldmine or angel invest in AI tools before they moon. Buying? It screams stability to boomers, but traps you in one zip code while opportunities scatter. This piece slices through the noise with hard 2024 data, raw pros and cons, and tailored scenarios for budgets from bootstrap to baller. Time to decide if you're building equity or an empire.

The 2024 Data Dump: Rents Rise, But Buying Bites Harder

Freddie Mac pegged average 30-year fixed rates at 6.12 percent as of early October, down a tick from summer peaks but still double pre-pandemic norms. Plug in $400,000 home, 20 percent down ($80,000), and you're servicing $2,100 monthly principal and interest alone, per Bankrate calculators. Add property taxes (1.1 percent national average), insurance ($150/month), and maintenance (1 percent of value yearly, or $333/month), and total ownership costs balloon past $3,200 monthly. Rents? CoreLogic's September tracker shows one-bedrooms averaging $1,650 nationwide, two-beds $2,000. In hot spots like Miami or Denver, expect $2,500+, but that's often all-in: no repairs, no equity roulette.

"Rents grew 3.4% YoY, outpacing wage growth in 90% of metros." - Apartment List, Sept 2024

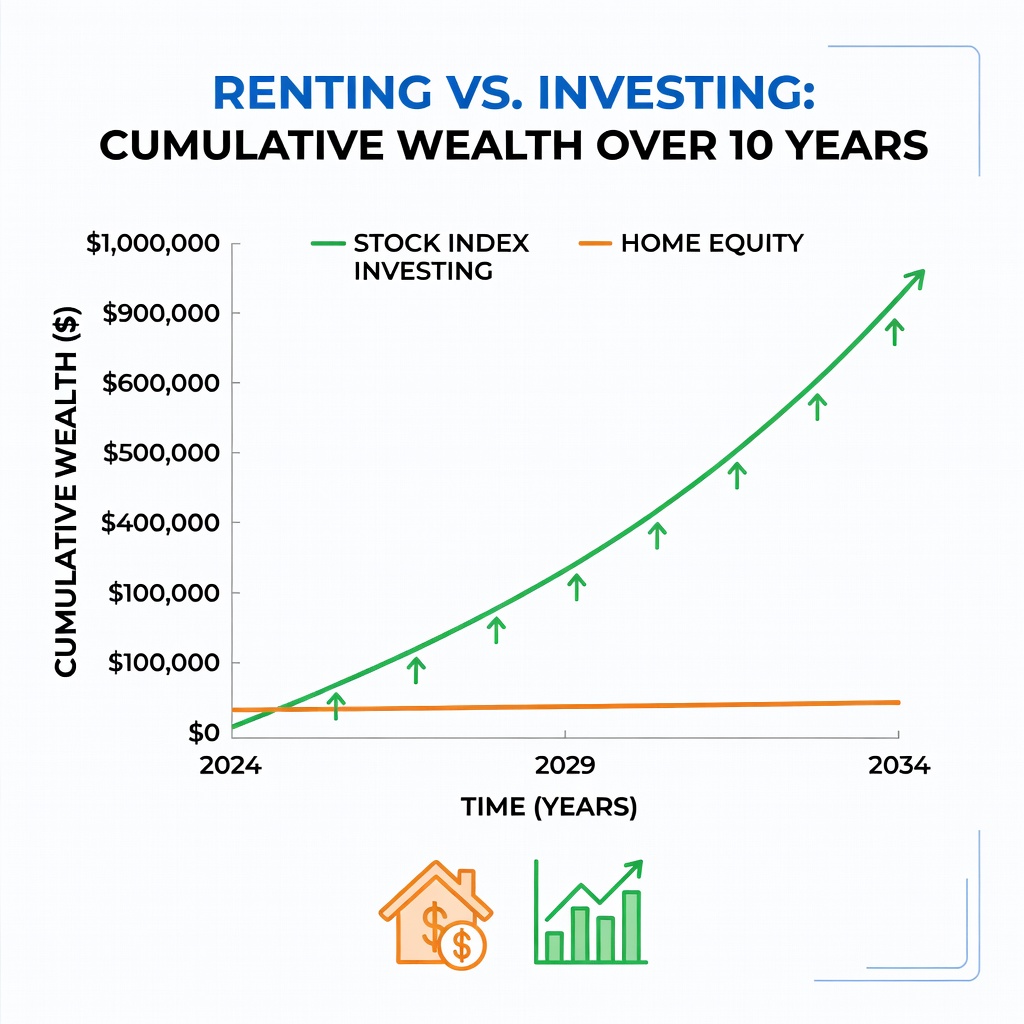

Inventory crunch persists; National Association of Realtors says active listings are 30 percent below 2019 levels, propping prices. Yet sales volume cratered 20 percent YoY. Translation: sellers hold firm, buyers balk at rates. Social media erupts with memes of 'houseless' millennials, but for Gen Z alphas grinding apps or e-com, renting's edge sharpens. A viral X thread from @FinancialSamurai last week tallied 15k likes: 'Rent, invest the delta in VOO, retire at 45.' Data backs it; Vanguard's S&P 500 ETF returned 25 percent annualized over five years, trouncing home appreciation's 5 percent clip.

Rent vs Buy: Pros, Cons, No Sugarcoating

Renting Wins: Flexibility reigns. Job offer in SF? Bail without realtor fees (5-6 percent of sale). Lifestyle perks: gym-equipped pads, rooftop pools, no mowing. Cash flow king, invest the spread. At 6.8 percent rates, that $1,200 monthly buy premium compounds to $220,000 in 10 years at 8 percent market returns (historical average). Tax perks minimal for singles; no mortgage interest deduction if income under $100k phases it out partially.

Renting Risks: No forced savings; discipline required or lifestyle creep eats gains. Landlord hikes or eviction roulette in tenant-unfriendly states like Texas. Inflation erodes purchasing power if wages lag.

Buying Wins: Leverage magic if prices soar; 3 percent annual appreciation on $320k leveraged equity builds wealth. Stability for families, though single grinders? Principal paydown acts like savings. Potential tax shields, fixed payments hedge inflation.

Buying Risks: Illiquid trap. Sell in downturn, lose 10 percent equity. Rates reset on ARM? Nightmare. Opportunity cost huge; that downpayment in Tesla stock could've 3x'd. Maintenance surprises drain bankrolls, per HomeAdvisor averages $17k/year decade one.

Pro Tip: Run NerdWallet's rent vs buy calculator weekly, rates fluctuate.Scenario 1: Bootstrap Budget ($4,000 Monthly Net, Entry-Level Hustle)

You're 24, software bootcamp grad, $65k salary plus Uber gigs netting $4k after taxes. Phoenix two-bed rent: $1,800. Leaves $1,400 play money after $800 basics. Buy? $350k condo, 10 percent down ($35k scraped from folks), PITI $2,400. Leftover: $800. Rent path: Max 401k, dump $800 into SCHD dividend ETF (4 percent yield). Five years: $60k portfolio. Buy path: $40k equity minus closing/repairs. Rent wins mobility; snag remote gig doubling pay.

Scenario 2: Mid-Tier Grinder ($7,000 Monthly Net, Corp Escapee)

27-year-old ex-FAANG, now indie consultant, $120k + bonuses. Nashville townhome rent $2,400. Buy $500k house, 20 percent down ($100k from prior savings), PITI $3,500. Rent surplus $1,100 vs buy $500. Invest in QQQ (Nasdaq ETF, 18 percent 5yr avg): $80k in 5 years. Buy builds $120k equity but ties you down. Priorities shift? Entrepreneurship calls; rent sublet, bootstrap SaaS. Social proof: @MrMoneyMustache X post, 'Rented 10 years, FI at 30 via index funds.'

Scenario 3: Baller Mode ($12,000+ Monthly Net, Serial Entrepreneur)

32, flipped e-com store, passive $200k/year. Miami penthouse rent $5k or $1.2m condo, 25 percent down ($300k cash), PITI $7k. Rent: $4k monthly investable into private equity or own rentals via Roofstock. Buy: Hedge against inflation, but diversify via REITs (VNQ up 12 percent YTD). Here, buy if location alpha (Airbnb cashflow), else rent nomad-style, chase VC in Austin.

The Escape Hatch: Hybrid Hustle Mindset

Forget binary; rent strategically in growth burbs (Austin 'burbs under $1,800), house hack spare room on Airbnb netting $1k/month. Stack skills: Learn RE investing via BiggerPockets forums, but start with Fundrise ($10 minimum crowdfunded deals). Entrepreneurship turbocharges; 40 percent millennials side-hustle per Bank of America, many quitting corp for freedom. Your edge: No DEI drag, pure merit grind.

Bottom line: 2024 math favors renting for most under 35. That $15k annual delta invested religiously? Millionaire by 45. Track via Excel dashboards, join Discords like WallStreetBets alts for tips. Ditch the debt dream; build the debt-free dynasty. What's your move?

Henry Wood

Henry focuses on lifestyle money choices like housing, cars, and travel, helping young readers weigh real-world tradeoffs behind big purchases.